Typical claim values for engineering and manufacturing

Engineering and manufacturing businesses tend to have higher average claim values than many other sectors — largely because the qualifying costs (materials consumed in prototype development and testing, specialist equipment time, engineer salaries) are often substantial. Typical annual claims range from £22,000 to £120,000, with businesses involved in bespoke product development or novel process design often at the higher end.

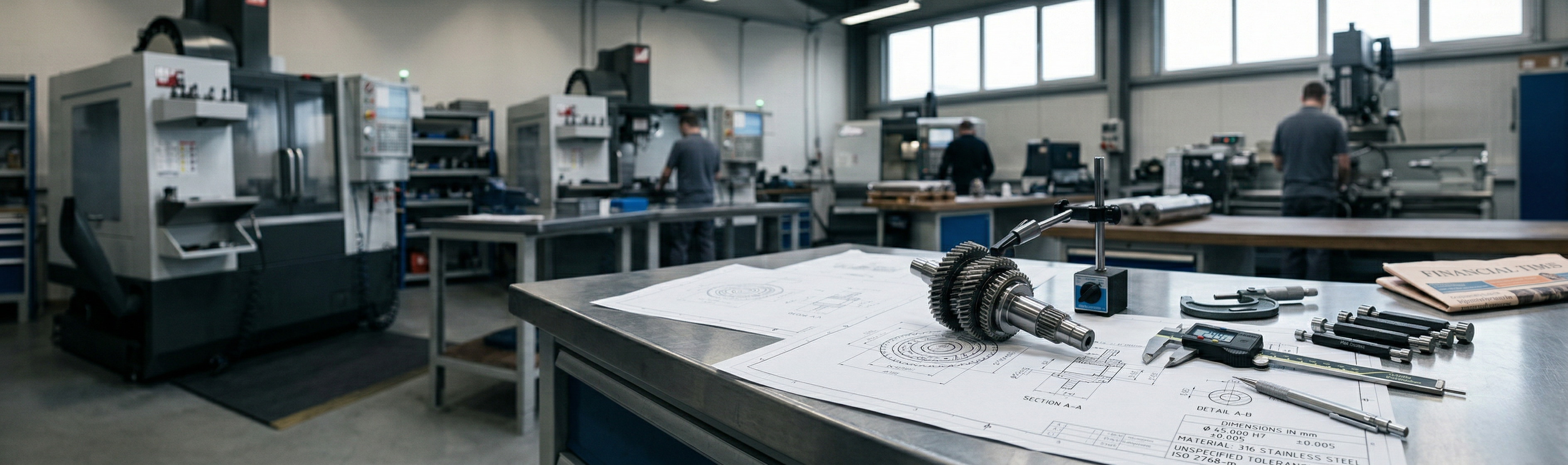

Three qualifying activity examples

Engineering and manufacturing R&D typically involves genuine technical uncertainty around materials, tolerances, process parameters, or performance characteristics. The following examples illustrate the kind of work that qualifies.

1. Developing a bespoke component to meet performance specifications no off-the-shelf part could satisfy

A precision engineering firm was asked to supply a component for an aerospace application requiring tolerances and material properties that no commercially available part could meet. The team spent four months designing, prototyping, and testing multiple iterations — consuming significant quantities of specialist alloy in the process. Each prototype revealed new failure modes that required design modifications. The uncertainty here is technical: the final design was not known at the outset, the outcome of each test was genuinely uncertain, and multiple approaches were tried before a solution was found. Staff time, materials consumed in testing, and subcontracted surface treatment costs all qualify. This is a textbook qualifying R&D project.

2. Adapting a manufacturing process for a new substrate with unpredictable behaviour

A manufacturer producing industrial coatings was asked to apply an existing protective process to a new composite material whose surface properties were significantly different from anything previously coated. The existing process parameters — temperature, dwell time, surface preparation chemistry — produced inconsistent results on the new substrate. The team conducted systematic trials across dozens of parameter combinations, working with a materials scientist to understand the adhesion mechanisms involved. Several months of iterative testing were required before a reliable process was established. The R&D here is in the systematic investigation: the uncertainty was real, the experimentation was structured, and the outcome was not predictable at the start.

3. Designing a novel jig or tooling solution for a production challenge with no known precedent

A contract manufacturer needed to hold an unusually complex fabricated assembly in precise alignment during a multi-stage welding process — a requirement for which no standard fixturing approach existed. The engineering team designed, built, and refined a custom jig over several iterations, each revealing distortion or alignment issues that required a redesign. The final solution involved a novel clamping mechanism that had not been used in this application before. The design time, material cost of the prototype jigs, and external toolmaking costs all qualify. What makes this R&D rather than routine engineering is the iterative nature of the process and the fact that the solution was not obvious to experienced toolmakers at the outset.

HMRC scrutiny level — medium

Engineering and manufacturing R&D claims sit in the medium scrutiny bracket. HMRC has long experience reviewing them and the sector's R&D is typically well-evidenced — engineers naturally produce technical documentation, test records, and design iteration logs that serve as contemporaneous evidence of R&D activity.

The most common scrutiny trigger in this sector is claims that include routine production work alongside genuine R&D, without clearly delineating between the two. A business that claims relief on the full salary cost of all engineering staff — including those working on standard production — is likely to face questions about apportionment methodology.

Common mistakes engineering businesses make

Including consumable materials used in production rather than in R&D. Consumables (materials consumed or transformed during the qualifying R&D process) are claimable — but only when they are used in the development or testing phase, not in the manufacture of finished goods for sale. A prototype that was built and tested but never sold qualifies. The same component manufactured as part of a production run does not, even if the design was novel.

Not claiming on subcontract testing and analysis costs. Engineering businesses frequently use external testing houses, metallurgical labs, or specialist analysis services during R&D projects. These costs qualify under the Merged Scheme (subject to the 65% restriction on unconnected subcontractors) — but many businesses assume only internal costs are claimable and leave significant qualifying expenditure unclaimed.

Underestimating the proportion of qualifying time. Engineers often spend a larger proportion of their time on genuinely uncertain technical problem-solving than they initially estimate. A careful review of project records frequently reveals that the qualifying proportion of time is higher than the first estimate — sometimes significantly so. Using a specialist adviser who understands how to conduct a thorough cost identification process consistently results in larger, more accurate claims.

Materials consumed in prototype development qualify even if the prototypes were ultimately unsuccessful. R&D that did not produce a working solution is still R&D — HMRC does not require a successful outcome, only a genuine attempt to resolve technological uncertainty.

Find out what your engineering business could claim

Free eligibility grader — 7 questions, personalised result, no registration required.